Four hundred and twenty-five days after the effectivity of the Corporate Recovery and Tax Incentives for Enterprises (CREATE) Act or Republic Act (RA) No. 11534 on April 11, 2021, one question still lingers among the registered business enterprises (RBEs) from the country’s nineteen Investment Promotion Agencies (IPAs): How can RBEs maximize their fiscal and non-fiscal incentives under the new tax rules and evolving market environment?

The key lies in the 2022 Strategic Investment Priority Plan (SIPP). Following the provisions under the CREATE Act, the SIPP refers to the priority projects or activities, including the scope and coverage of location and industry tiers, determined by the Board of Investments (BOI), in coordination with the private sector, Fiscal Incentives Review Board (FIRB), IPAs, and other government agencies administering tax incentives.

Prior to the effectivity of the CREATE Act and the 2022 SIPP, the 2020 Investment Priorities Plan (IPP) issued on November 18, 2020, lists the industries and activities that may be subject to fiscal and non-fiscal incentives.

The newly formulated 2022 SIPP is aligned with the goals, priorities, and strategies of the revised Philippine Development Plan 2017-2022 and the development agenda and strategy of the DTI and DOST. It continues to adopt the projects or activities in the 2020 IPP, while expanding the priority list to address the growing concern on climate change, economic and medical challenges in managing the COVID-19 pandemic, international and local security relations, and lack of innovation and technological advancements.

What are the projects or activities under the 2022 SIPP?

The CREATE Act introduced fiscal and non-fiscal incentives in tiers such that the qualified projects or activities are also categorized in industry tiers. Tier 1 covers all activities listed in the 2020 IPP, unless specifically listed under Tiers 2 or 3. Tier 2 covers all activities that address value chain gaps and promote green ecosystems, dependable health systems, and self-reliant defense systems. Tier 3 covers all activities that focus on the application of research and development and attracting technology investments. The table below summarizes the projects or activities:

![]()

The 2022 SIPP excluded RBEs engaged in customs brokerage, trucking or forwarding services, janitorial services, security services, insurance, banking and other financial services, consumers’ cooperatives, credit unions, consultancy services, retail enterprises, restaurants, public administration, or such other similar services. Further, it is projected that at least 30% of the gross domestic product earned in the National Capital Region (NCR) will be reallocated to provincial areas.

The list of priority projects or activities detailed in the 2022 SIPP is not entirely new. Similarities can be found in the IPPs from prior years. The 2014-2016 IPP included regional dispersal of industries and locational restriction in NCR, creation of specialty hospitals, and manufacture of alternative fuel vehicles, while the 2017-2019 IPP emphasized research and development activities, commercialization of new and emerging technologies, and climate change–related projects.

The 2022 SIPP is effective June 11, 2022, or 15 days after the date of publication in a newspaper of general circulation, and is valid for three years until June 10, 2025, subject to review and amendment every three years thereafter, unless a supervening event necessitates an earlier review.

What do RBEs stand to gain under the 2022 SIPP?

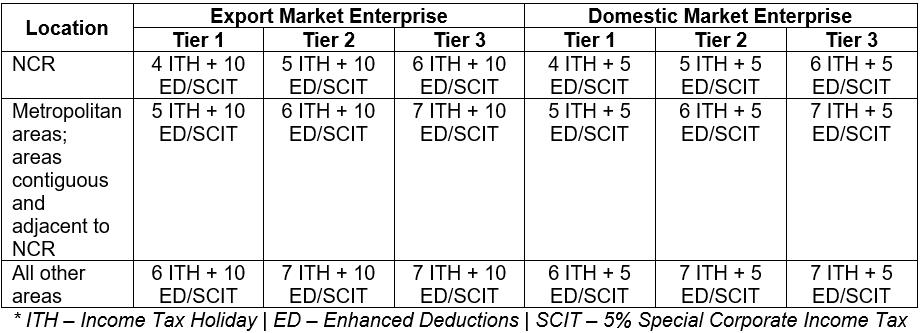

RBEs can either be export market enterprise or domestic market enterprise, depending on its total export commitment. Export market enterprises refer to RBEs that export at least 70% of its total revenue or production output while domestic market enterprises refer to RBEs that export below the minimum threshold for export enterprises.

Regardless of which IPA the RBEs will apply, the period of availment of incentives is based on the combination of location and industry summarized as follows:

![]()

In addition, qualified RBEs enjoy duty exemption on importation of capital equipment, raw materials, spare parts or accessories, and value-added tax (VAT) exemption on importation and VAT zero-rating on local purchases that are directly and exclusively used in the registered activity of the RBEs.

As such, the farther the RBEs are located from metropolitan areas and the more the projects or activities involve research and development applications and highly advanced technologies, the higher are the incentives.

How can RBEs maximize its fiscal and non-fiscal incentives under the new tax rules and evolving market environment?

It is prudent for the RBEs to weigh the pros and cons on whether to continue with their status quo, restructure their business model, or transfer their registration to another IPA or location. A carefully laid out tax study may prove beneficial in assessing the best option that is most suitable to the RBE in the long run.

What’s next for RBEs?

Investment prospects in the Philippines remain robust. According to the Philippine Statistics Authority, total approved foreign and Filipino investments in the first quarter of 2022 increased to P190.87 billion as compared to P164.9 billion in the same quarter of 2021. The BOI approved 95% of the total investments, representing a 32% increase from the first quarter of 2021. On the other hand, investments approved by PEZA decreased by 68% from 25 billion in the first quarter of 2021 to P8 billion in the first quarter of 2022.

The top three projects or activities pertain to electricity and gas, real estate activities, and manufacturing while the top three investing countries are Japan, South Korea, and Singapore.

With the effectivity of the 2022 SIPP, the issuance of synchronized implementing regulations from various concerned government agencies is necessary in addressing gray areas. These include the criteria and guidelines on green ecosystems and artificial intelligence projects. Priority must also be given to expediting the setting up and conduct of registered projects or activities, anchored on the principles of Ease of Doing Business and Efficient Government Service Delivery Act of 2018. One of the salient features under the amended Foreign Investment Act (RA No. 11647) is the creation of an Inter-Agency Investment Promotion Coordination Committee among the IPAs. This Committee will promote a unified and efficient approach on evaluation of investments and granting of incentives for RBEs.

So, to all the RBEs, stay vigilant as interesting developments will be rolled out in the foreseeable future.

Let's Talk Tax is a weekly newspaper column of P&A Grant Thornton that aims to keep the public informed of various developments in taxation. This article is not intended to be a substitute for competent professional advice.

As published in BusinessWorld, dated 21 June 2022