-

Audit approach overview

Our audit approach will allow our client's accounting personnel to make the maximum contribution to the audit effort without compromising their ongoing responsibilities

-

Annual and short period audit

At P&A Grant Thornton, we provide annual and short period financial statement audit services that go beyond the normal expectations of our clients. We believe strongly that our best work comes from combining outstanding technical expertise, knowledge and ability with exceptional client-focused service.

-

Review engagement

A review involves limited investigation with a narrower scope than an audit, and is undertaken for the purpose of providing limited assurance that the management’s representations are in accordance with identified financial reporting standards. Our professionals recognize that in order to conduct a quality financial statement review, it is important to look beyond the accounting entries to the underlying activities and operations that give rise to them.

-

Other Related Services

We make it a point to keep our clients abreast of the developments and updates relating to the growing complexities in the accounting world. We offer seminars and trainings on audit- and tax-related matters, such as updates on Accounting Standards, new pronouncements and Bureau of Internal Revenue (BIR) issuances, as well as other developments that affect our clients’ businesses.

-

Tax advisory

With our knowledge of tax laws and audit procedures, we help safeguard the substantive and procedural rights of taxpayers and prevent unwarranted assessments.

-

Tax compliance

We aim to minimize the impact of taxation, enabling you to maximize your potential savings and to expand your business.

-

Corporate services

For clients that want to do business in the Philippines, we assist in determining the appropriate and tax-efficient operating business or investment vehicle and structure to address the objectives of the investor, as well as related incorporation issues.

-

Tax education and advocacy

Our advocacy work focuses on clarifying the interpretation of laws and regulations, suggesting measures to increasingly ease tax compliance, and protecting taxpayer’s rights.

-

Business risk services

Our business risk services cover a wide range of solutions that assist you in identifying, addressing and monitoring risks in your business. Such solutions include external quality assessments of your Internal Audit activities' conformance with standards as well as evaluating its readiness for such an external assessment.

-

Business consulting services

Our business consulting services are aimed at addressing concerns in your operations, processes and systems. Using our extensive knowledge of various industries, we can take a close look at your business processes as we create solutions that can help you mitigate risks to meet your objectives, promote efficiency, and beef up controls.

-

Transaction services

Transaction advisory includes all of our services specifically directed at assisting in investment, mergers and acquisitions, and financing transactions between and among businesses, lenders and governments. Such services include, among others, due diligence reviews, project feasibility studies, financial modelling, model audits and valuation.

-

Forensic advisory

Our forensic advisory services include assessing your vulnerability to fraud and identifying fraud risk factors, and recommending practical solutions to eliminate the gaps. We also provide investigative services to detect and quantify fraud and corruption and to trace assets and data that may have been lost in a fraud event.

-

Cyber advisory

Our focus is to help you identify and manage the cyber risks you might be facing within your organization. Our team can provide detailed, actionable insight that incorporates industry best practices and standards to strengthen your cybersecurity position and help you make informed decisions.

-

ProActive Hotline

Providing support in preventing and detecting fraud by creating a safe and secure whistleblowing system to promote integrity and honesty in the organisation.

-

Accounting services

At P&A Grant Thornton, we handle accounting services for several companies from a wide range of industries. Our approach is highly flexible. You may opt to outsource all your accounting functions, or pass on to us choice activities.

-

Staff augmentation services

We offer Staff Augmentation services where our staff, under the direction and supervision of the company’s officers, perform accounting and accounting-related work.

-

Payroll Processing

Payroll processing services are provided by P&A Grant Thornton Outsourcing Inc. More and more companies are beginning to realize the benefits of outsourcing their noncore activities, and the first to be outsourced is usually the payroll function. Payroll is easy to carve out from the rest of the business since it is usually independent of the other activities or functions within the Accounting Department.

-

Our values

Grant Thornton prides itself on being a values-driven organisation and we have more than 38,500 people in over 130 countries who are passionately committed to these values.

-

Global culture

Our people tell us that our global culture is one of the biggest attractions of a career with Grant Thornton.

-

Learning & development

At Grant Thornton we believe learning and development opportunities allow you to perform at your best every day. And when you are at your best, we are the best at serving our clients

-

Global talent mobility

One of the biggest attractions of a career with Grant Thornton is the opportunity to work on cross-border projects all over the world.

-

Diversity

Diversity helps us meet the demands of a changing world. We value the fact that our people come from all walks of life and that this diversity of experience and perspective makes our organisation stronger as a result.

-

In the community

Many Grant Thornton member firms provide a range of inspirational and generous services to the communities they serve.

-

Behind the Numbers: People of P&A Grant Thornton

Discover the inspiring stories of the individuals who make up our vibrant community. From seasoned veterans to fresh faces, the Purple Tribe is a diverse team united by a shared passion.

-

Fresh Graduates

Fresh Graduates

-

Students

Whether you are starting your career as a graduate or school leaver, P&A Grant Thornton can give you a flying start. We are ambitious. Take the fact that we’re the world’s fastest-growing global accountancy organisation. For our people, that means access to a global organisation and the chance to collaborate with more than 40,000 colleagues around the world. And potentially work in different countries and experience other cultures.

-

Experienced hires

P&A Grant Thornton offers something you can't find anywhere else. This is the opportunity to develop your ideas and thinking while having your efforts recognised from day one. We value the skills and knowledge you bring to Grant Thornton as an experienced professional and look forward to supporting you as you grow you career with our organisation.

Revised Minimum Capitalization, Financial Capacity, and Other Regulatory Requirements for HMOs

Background

The Health Maintenance Organization (HMO) industry has experienced significant growth in membership and services and is expected to play a larger role in the national healthcare system, necessitating updates to the regulatory framework to ensure financial stability, operational efficiency, and inclusivity in delivering healthcare to a broader population.

In recognition of the Insurance Commission's (IC) objective to establish progressive regulatory and supervisory policies over the HMO industry, the IC sees the need to revise the rules and regulations that govern the minimum capitalization and financial capacity requirements for HMOs.

In view of the foregoing, following revised minimum capitalization, financial capacity, and other regulatory requirements for HMOs are hereby promulgated by the IC:

Section 1: Coverage

This Circular Letter (CL) covers the revised rules and regulation regarding HMO's minimum capitalization and financial capacity requirements.

Section 2: Minimum Capitalization and Financial Capacity

Paid-up Capital

- All existing domestic HMOs must have a minimum paid-up capital of at least P10,000,000.

- No new HMO shall, in a stock corporation, engage in the business of HMO in the Philippines unless it has a paid-up capital of at least P100,000,000.

- Community-based and cooperative HMOs shall maintain a paid-up capital equivalent to 50% of what is prescribed for a regular HMO.

- In case of a foreign HMO applying for an HMO branch license, no license shall be issued unless the branch has a statutory deposit of an amount equal to the prevailing minimum paid-up capital for domestic HMOs in cash and/ or allowable securities approved by the IC.

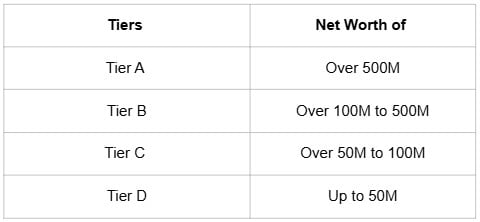

Net Worth

- All HMOs must maintain a net worth that is not lower than their actual paid-up capital. Additionally, HMOs shall be classified into the following categories based on their net worth:

- In the examination of HMO's financial condition, assets of doubtful economic value and/or unsupported shall be considered unaccounted. Liabilities not set up in the books as of a given accounting period shall be treated as non-ledger liabilities.

- If it is found that the net worth is less than the amount as required in this CL, the same shall be fully covered with a cash infusion to be contributed proportionately by the stockholders on record within fifteen (15) days of receipt of the advice from the IC.

Security Deposit

- Every HMO doing business in the Philippines shall at all times maintain a security deposit of at least 25% of the actual paid-up capital or P5,000,000, whichever is higher.

- The security deposit shall be invested only in bonds or other debt instruments of the Government of the Philippines, its political subdivisions or instrumentalities, or government-owned or -controlled corporations and entities, including the Bangko Sentral ng Pilipinas (BSP), with a maturity of at least 1 year from the date of transfer to the IC.

- The investment shall at all times be maintained free from any lien or encumbrance.

- The government securities must be lodged as regulatory compliance under the lC's NRoSS account, ICRCPHMM999.

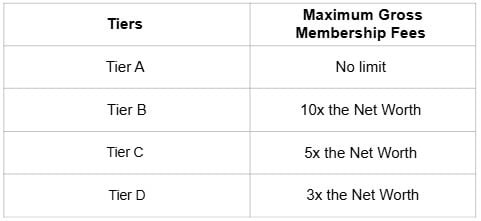

Risk-based Capitalization

- All HMOs must maintain a net worth that is not lower than their actual paid-up capital. Additionally, HMOs shall be classified into the following categories based on their net worth:

For this purpose, gross membership fees pertain to the total annual fees arising from full-risk HMO agreements of the pre-agreed set of health services.

- If upon examination, it is found that the total risk on membership fees exceeds the above Maximum Gross Membership Fees as required in this CL, the same shall be fully covered by cash infusion to be contributed proportionately by the stockholders on record within 15 days from receipt of notice from the IC.

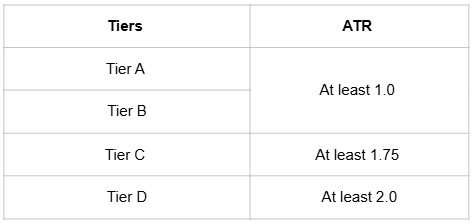

Liquidity

- Depending on the tier, HMOs shall at all times maintain an Acid Test Ratio (ATR) based on the following:

ATR shall be computed using the following formula: ATR = Quick Assets / Current Liabilities

- If upon examination of the HMO's financial condition, it is found that the ATR is less than the required ratio in this CL, HMOs may collect its long-term receivables and/or liquefy non-current assets or infuse cash to be contributed proportionately by the stockholders on record within 15 days from receipt of notice from the IC.

Investment in Real Estate Properties

- HMOs classified under Tiers A, B, and C are allowed to invest in real estate properties.

- Valuation of real estate properties requires prior approval from the IC and shall be conducted by an accredited appraiser of the Securities and Exchange Commission (SEC).

- For examination purposes, any investment in real properties by an HMO under Tier D shall be considered unaccounted. Further, revaluation increments for real estate properties with no lC-approved valuation shall be considered unaccounted.

Cash Infusion

- Any cash infusion by the stockholders to cover any impairment or deficiency in net worth, liquidity, and RBC may be recorded as "Contingency Surplus" in the HMO's equity accounts. This account can be withdrawn only upon prior written approval by the IC. (Annex A of CL No. 2018-68 shall be amended to include "Contingency Surplus" in the net worth accounts of the Statement of Financial Position)

- HMOs that infused cash to cover any deficiency resulting from the IC's examination of the 2023 Audited Financial Statements (AFS) and Interim Financial Statements may be allowed to reclassify the cash infusion to Contingency Surplus, subject to the approval of the IC.

Dividend Distribution

- HMOs classified under Tiers C and D must secure prior approval or clearance from the IC before declaring dividends. If the IC finds that any HMO under these tiers has declared or distributed dividends without the IC's approval, it may order such HMO to cease and desist from doing business until the amount of such dividend, or the portion thereof, has been restored to said HMO.

- HMOs under Tiers A and B may declare dividends without such approval subject to the Post-Distribution Reportorial Requirements.

Section 3: Prudential Reporting and Disclosure

Disclosure Requirement

- ln addition to the disclosures required under PFRS Accounting Standards, HMOs shall present information on their compliance with the minimum capitalization and financial capacity requirements specified in Section 2 of this CL in a separate supplemental report to the annual financial statements, following the lC-prescribed template.

Reportorial Requirements

- Audited Financial Statements

- All HMOs are required to submit their AFS for the year ending December 31 and other required documents or attachments on or before May 31 of the following year, in accordance with lC CL No. 2025-08.

- A filing fee of P20,000 plus P200 representing Legal Research Fund (LRF) shall be imposed upon submission of the AFS and P5,000 for every calendar day of delayed submission.

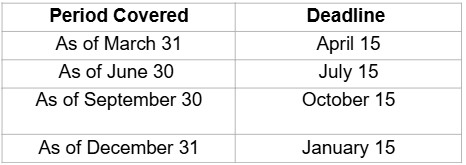

- Interim Financial Statements

- Additionally, all HMOs must submit their IFS in accordance with lC CL No 2019-43, following the schedule below:

HMOs that fail to submit their IFS based on the respective deadlines shall be subject to a basic fine of P5,000 and P500 for every calendar day of delayed submission.

- Documentary Requirements for Security Deposit

- HMOs that have purchased government securities in compliance with security deposit requirements shall report the same to the IC through the Investment Services Division within the day of transfer of securities. The report shall be accompanied by:

i. Certified True Copy of Confirmation of Sale of securities from the bank

ii. Notarized Affidavit of Undertaking

iii. Notarized Deed of Assignment with Special Power of Attorney

iv. Certification on Compliance with the Security Deposit Requirement

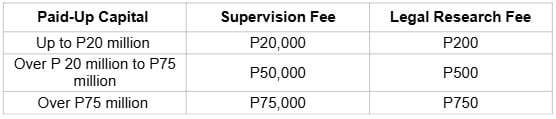

Section 4: Supervision Fee

HMOs are required to pay the annual supervision fee, which is due on or before March 1 of each year and shall be collected based on the following:

HMOs that fail to pay the required fee will be subject to a basic fine of P5,000, plus an additional P500 for each calendar day the payment is delayed.

Effectivity

Unless otherwise provided, the provisions of this CL shall take effect immediately.

Please see attached circular for further guidance.